Asia-Pacific PC shipments seen falling 13.7% in 2026

Thu, 26th Mar 2026

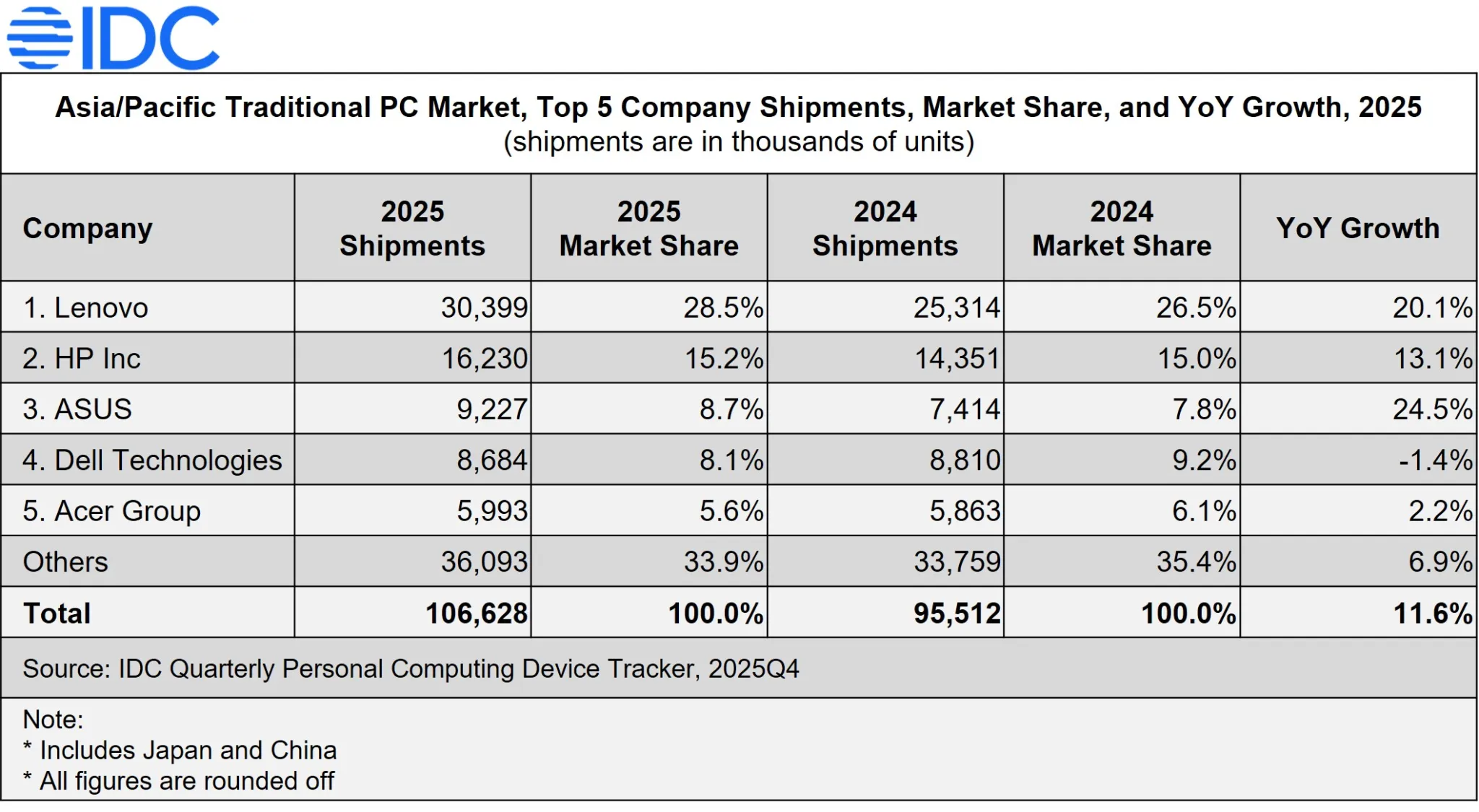

Asia-Pacific PC shipments grew 11.6% in 2025, but IDC expects them to fall 13.7% in 2026.

Traditional PC shipments across Asia-Pacific, including Japan and China, reached 106.6 million units in 2025, spanning desktops, notebooks and workstations. IDC projects that total to fall to 92.0 million units in 2026 as component shortages and higher prices weigh on both supply and demand.

Growth in 2025 was driven by replacement demand for ageing devices ahead of the end of support for Windows 10. Large education purchases in markets such as India, Indonesia and Japan also lifted volumes.

All countries in the region posted year-on-year shipment growth in the fourth quarter of 2025, as vendors and customers brought forward orders and procurement amid concerns over tighter supply and higher prices in 2026.

Consumer demand remained positive across much of the region, though not everywhere. The consumer PC market grew 6.4% to 50.1 million units, with desktop shipments up 4.4% and notebook shipments up 7.0%.

Hong Kong and Korea were exceptions, recording declines in 2025 as weaker demand offset broader improvements in consumer sentiment elsewhere in the region.

The commercial segment expanded faster, with shipments rising 16.7% to 56.6 million units. Desktop shipments increased 8.9%, notebooks 24.0% and workstations 6.8%.

Business demand was supported by replacement cycles for devices bought during the pandemic and continued migration to Windows 11. Public sector buying also rose sharply, with education and government both posting strong double-digit annual growth, according to IDC.

Supply pressure

The expected reversal in 2026 reflects supply and pricing pressures as well as weaker underlying demand after the recent refresh cycle. Shortages in key components and rising prices are likely to affect both the availability of new systems and buyers' willingness to spend.

Memory is a key pressure point. Strong demand linked to artificial intelligence infrastructure is tightening global supplies of DRAM and NAND, as manufacturers shift production toward data-centre requirements and away from consumer electronics.

That shift is making it harder for PC makers to secure the memory needed for new machines. IDC expects the shortages to push prices higher, which could curb demand across the region after the strong rebound in 2025.

Matthew Ong, Senior Market Analyst, Devices Research, IDC Asia/Pacific, said the region's broad-based growth in 2025 was driven by refresh demand and education deployments, while the late-year surge reflected efforts to get ahead of expected supply constraints and price increases in 2026.

"In 2025, the Asia/Pacific* region recorded growth across all segments, driven by a strong refresh demand to replace aging devices in conjunction with the Windows 10 end of support and large-scale education deployments in countries such as India, Indonesia, and Japan. All countries in the region recorded YoY shipment growth in the fourth quarter of 2025, as vendors and end users accelerated shipments and procurement in anticipation of supply constraints and price increases in 2026," said Ong.

Regional divide

IDC expects the impact of tighter supply and higher costs to vary across Asia-Pacific. Vendors are likely to focus on mature markets with higher average selling prices to protect margins.

That could leave emerging markets more exposed to shortages and price increases. Southeast Asian countries in particular may face greater pressure because they rely more heavily on lower-end devices and buyers there are more sensitive to price changes.

Maciek Gornicki, Senior Research Manager, Devices Research, IDC Asia/Pacific, said the supply imbalance extends well beyond the PC industry.

"Strong demand driven by AI infrastructure is creating significant constraints in the global supply of DRAM and NAND as memory manufacturers shift production capacity away from consumer electronics to meet growing data-center needs. This is disrupting PC supply, with vendors struggling to secure the memory components needed to build new systems. We expect these shortages to drive prices higher and soften overall demand. In Asia/Pacific, vendors are anticipated to prioritize mature markets with higher ASPs to protect margins, while emerging economies-particularly Southeast Asia-will face the greatest impact from both product shortages and rising prices, as these markets are more reliant on lowend devices and consumers are especially sensitive to cost increases," said Gornicki.